Trump’s Iran Peace Deal: A Historic Opening, or the Next War in Disguise?

The Week That Shaped the World — 12 – 19 June 2026

Trump’s Iran Peace Deal Tests the World’s Faith in Fragile Stability — and Other Major Stories of the Week

There are weeks when history moves loudly. Then there are weeks when it signs a peace deal, moves oil prices, frightens central bankers and quietly feeds another rally in artificial intelligence stocks.

Trump’s interim agreement with Iran offered the world a rare diplomatic pause: lower anxiety around the Strait of Hormuz, a possible path away from wider Middle Eastern war, and the kind of market relief investors are always ready to mistake for stability.

But the calm was never clean. Israel remains unwilling to stand down. The proposed $300 billion reconstruction mechanism looks, to this magazine, uncomfortably close to reparations in softer clothing. Ukraine brought the war closer to Moscow. The World Bank cut its global growth outlook. The Fed rediscovered inflation fear. And tech investors rushed back into AI as if peace itself had become part of the infrastructure trade.

“Peace is no longer merely a diplomatic condition. It is a market instrument — and a very fragile one.”

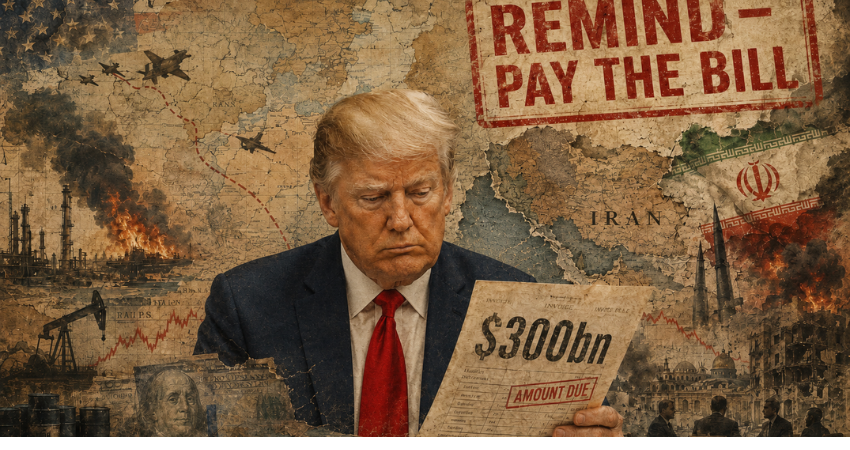

1. Trump’s Iran Peace Deal: A Historic Opening, or the Next War in Disguise?

For a brief moment this week, the Middle East looked as if it had remembered how to breathe.

The United States and Iran moved towards an interim peace arrangement designed to stop the war, reopen the Strait of Hormuz and create a 60-day window for a more permanent settlement. Oil markets relaxed. Diplomats rediscovered their favourite vocabulary. Words such as “breakthrough”, “stability” and “de-escalation” returned to the table, as if language itself could clean the blood from the floor.

And yes, this matters.

Any agreement capable of stopping missiles, reopening one of the world’s most important energy corridors and preventing another generation from growing up under the shadow of strategic madness deserves to be recognised as a positive moment in history. If this deal holds, even partially, it could become one of those rare diplomatic pauses in which the region steps back from the edge and remembers that survival is also a policy.

But Prime Economist would be failing its readers if it confused a signed document with peace.

The first problem is Israel. For Washington, the deal may look like statecraft. For Tehran, it may look like breathing space. For the oil market, it is simply a return to something resembling predictability. But for Benjamin Netanyahu, Iran is not a market event, nor a diplomatic puzzle, nor a useful line in Trump’s campaign mythology. Iran remains the central threat around which Israel’s security doctrine has been built.

That is why this fragile peace already looks almost certain to be broken — or at least pushed to the edge — by Israel’s next move. Netanyahu has little political room to accept an agreement that leaves Iran standing, breathing and rebuilding. If Trump has signed a pause, Israel may still be preparing the continuation.

Then there is the money.

Officially, the proposed $300 billion reconstruction fund is not reparations. The language is softer, cleaner, more suitable for diplomatic carpets and post-war handshakes. It is presented as reconstruction, stabilisation, regional responsibility — all the respectable words usually brought out when nobody wishes to admit what has really been purchased.

But Prime Economist sees something else here. Not a legal admission, perhaps. Not a signed confession. But something that, with a rather high degree of probability, resembles reparations in exchange for peace.

The money may not come directly from Washington. The cheque may be passed through Gulf capitals, investment vehicles and recovery mechanisms. Still, the political shape is difficult to ignore. A war is launched under the banner of nuclear danger. Its declared objectives remain, at best, blurred. Then comes a vast financial mechanism designed to make Iran whole enough to accept the settlement and quiet enough to reopen the Strait of Hormuz. One may call that reconstruction. Adam Jenkins would call it a very expensive way of leaving the room without saying sorry.

There is another uncomfortable question. Was this war ever only about Iran’s nuclear programme? Or was it also about leverage — over oil, shipping lanes, political optics and the theatre of global markets?

This is not an accusation. It is an editorial hypothesis. But when one man’s sentence can move crude prices, calm equities or panic the Strait of Hormuz, the border between diplomacy and market power becomes dangerously thin. If those close to power understand the rhythm of escalation before the market does, then oil ceases to be merely a commodity. It becomes information with a price attached.

That is the uglier shadow behind this week’s apparent breakthrough. Trump can sell the deal as statesmanship. Iran can sell it as resistance rewarded. Gulf states can sell it as regional stabilisation. Markets can pretend the crisis has been priced in and safely filed away.

But the Middle East rarely obeys neat endings. Peace has been announced. Money has been dressed in diplomatic language. Israel is already restless. And the Strait of Hormuz, that narrow throat through which so much of the world’s energy still passes, remains one speech, one strike, one miscalculation away from becoming a weapon again.

So yes, this may be a historic opening.

But history has a bad habit of laughing at men who mistake a ceasefire for peace.

“The most dangerous peace deals are not the ones signed in bad faith. They are the ones signed while the next war is already waiting in the corridor.”

2. Israel’s Refusal to Stand Down: The Peace Deal Meets Its First Real Enemy

Every peace agreement has two lives. One exists on paper, where the language is calm, symmetrical and very pleased with itself. The other begins the moment soldiers, politicians and frightened civilians are asked to behave as if the paper has changed reality.

This week, the US–Iran peace arrangement met its first real enemy: Israel’s refusal to treat the deal as the end of the matter.

For Donald Trump, the agreement can be sold as the great pause — a statesman’s intervention, a market-calming act, perhaps even the beginning of a wider Middle Eastern settlement. For Tehran, it offers economic breathing space and a chance to present survival as victory. But for Benjamin Netanyahu, the deal appears to solve Washington’s problem while leaving Israel’s problem very much alive.

That problem is Iran’s regional reach. Hezbollah in Lebanon. Iranian influence across the region. The military infrastructure that Israel believes cannot simply be negotiated away by a memorandum signed somewhere else.

This is where the entire diplomatic construction begins to look dangerously thin.

Israel has little incentive to accept a peace framework that leaves Hezbollah armed, Iran politically intact and southern Lebanon unresolved. Netanyahu can hardly return to the Israeli public and say that Washington has decided the war is over, therefore Israel must now be quiet. That may satisfy a press conference. It does not satisfy a security doctrine built on pre-emption, pressure and the refusal to wait for threats to become convenient.

Prime Economist’s view is that this fragile peace will almost certainly be tested — and possibly broken — not by the formal collapse of US–Iran diplomacy, but by Israel’s next operation. One strike. One retaliation. One expanded security zone. One attack answered by another attack. That is often how peace dies in the Middle East: not with a declaration, but with a military necessity wrapped in national survival.

There is, of course, a brutal logic to Israel’s position. No state wants to outsource its security to a deal it did not design and does not fully trust. But there is also a wider danger. If every actor keeps the right to continue fighting after peace has been announced, then the agreement becomes less a settlement than a pause between explosions.

Trump may have signed a diplomatic achievement. But Netanyahu holds one of the matches.

And in this region, that is rarely a minor detail.

“A peace deal is only as strong as the first country willing to ignore it in the name of survival.”

3. G7 in France: The West Tries to Manage Four Crises at Once

There was something almost theatrical about this year’s G7 summit in France. The setting was elegant, the photographs carefully composed, the language polished in that familiar diplomatic way — firm enough to sound serious, vague enough to survive the evening.

But behind the smiles, the agenda looked less like a summit and more like a damage-control operation.

Iran. Ukraine. China. Artificial intelligence.

Four crises, one table.

The leaders gathered in Évian-les-Bains at a moment when the world economy was no longer being disturbed by isolated shocks, but by overlapping systems of pressure. The war in the Middle East was moving oil. Oil was moving inflation. Inflation was moving central banks. Ukraine was still bleeding through Europe’s security architecture. China’s grip on critical minerals remained one of the great strategic chokeholds of the century. And AI, once sold as a bright productivity miracle, was increasingly becoming a question of power, energy, infrastructure and control.

Naturally, the G7 produced the appropriate words.

Support for Ukraine. Caution on Iran. Concern over China’s dominance in critical minerals. A renewed discussion about AI governance, safety and responsibility. The sort of language that looks reassuring until one remembers that reassurance is not the same as control.

The critical minerals discussion may prove to be the most practical part of the summit. Lithium, nickel, rare earths and other strategic materials are no longer just industrial inputs. They are the quiet skeleton of the new economy — the stuff beneath batteries, defence systems, data centres, semiconductors and the green transition. Whoever controls supply does not merely sell materials. They influence the speed at which everyone else can modernise.

That is why the G7’s attempt to coordinate policy, data-sharing and crisis response around mineral supply chains matters. It is not glamorous. It will not produce heroic headlines. But it is exactly the kind of boring institutional work that decides whether the West remains strategically independent or spends the next decade discovering that every “new economy” still begins with someone else’s mine.

Then came AI.

The presence of leading technology executives around the summit was a reminder that artificial intelligence is no longer a Silicon Valley story. It is now diplomacy with server farms attached. Governments are no longer asking only whether AI is safe. They are asking who builds it, who powers it, who regulates it, who profits from it — and, perhaps most quietly, who becomes dependent on it.

This is the deeper meaning of the summit. The G7 is no longer simply managing the old world of trade, armies and alliances. It is trying to govern a new one where oil prices, drone wars, mineral chokepoints and machine intelligence all belong to the same strategic map.

And that map is becoming harder to read.

Trump left France able to present himself as the man at the centre of everything: Iran, Ukraine, markets, minerals, AI. Europe left still searching for leverage. Canada, Japan and Britain left with the familiar problem of supporting the architecture without fully commanding it. And China, though absent from the room, remained present in almost every serious conversation.

That may be the uncomfortable lesson of this G7. The West can still gather, speak and coordinate. It can still produce statements, frameworks and platforms. But the world it is trying to manage has become faster, harsher and less obedient than the institutions built to manage it.

The summit did not fail.

But it did remind us how much global leadership now looks like trying to repair the roof while the house is already shaking.

“The G7 still knows how to write communiqués. The harder question is whether the world still waits long enough to read them.”

4. Ukraine Brings the War to Moscow: The Refinery That Burned Too Close to the Kremlin

For most of this war, Moscow has lived with a strange privilege: the capital of an invading state, yet not quite a city at war.

That illusion took another blow this week.

Ukrainian drones struck the Moscow oil refinery in Kapotnya, in the south-east of the city, for the second time in a matter of days. There were explosions, fire, black smoke, disrupted flights and the familiar official language of control. The refinery was not just another industrial site. It is a major fuel supplier for the Moscow region, part of the energy bloodstream that keeps the capital moving while the war burns elsewhere.

Now that bloodstream has become a target.

This was not merely a symbolic attack, though the symbolism is difficult to miss. A refinery burning within reach of the Kremlin’s political imagination sends a message that no communiqué can quite soften: the war has learned the road to Moscow. Not to Red Square, not to the polished theatre of state power, but to the infrastructure beneath it — fuel, logistics, aviation, supply, nerves.

That is where the economic meaning lies.

Ukraine has increasingly treated Russia’s energy system as a battlefield in its own right. Oil refineries, depots and fuel infrastructure are not only industrial assets. They are revenue channels, military enablers and psychological anchors. Strike them often enough, and the damage is not measured only in flames. It appears in repair costs, supply disruptions, insurance risk, fuel prices, air traffic interruptions and the uncomfortable sense that distance no longer protects the centre.

Moscow, of course, will present the attack as terrorism. Kyiv will present it as strategic retaliation against a state that has spent years bombing Ukrainian cities, power stations and civilian infrastructure. Both narratives will be used because both sides understand that modern war is fought not only with drones, but with interpretation.

Prime Economist’s view is colder.

This strike marks another stage in the industrialisation of long-range drone warfare. Ukraine is no longer merely defending territory with Western weapons and courage. It is building a capacity to reach into Russia’s economic machinery and make the cost of war more visible to those who were supposed to remain spectators.

That does not mean the attack will force peace. If anything, it may provoke another round of Russian missile and drone strikes against Ukrainian cities. War has a miserable habit of answering damage with damage, as if repetition were strategy.

But something has changed.

For years, Russia tried to make Ukraine feel that nowhere was safe. This week, Ukraine returned the lesson — not through rhetoric, not through diplomacy, but through fire over Moscow’s fuel supply.

The consequences may not be immediate. Refineries can be repaired. Flights can resume. Smoke can clear. Officials can speak confidently again.

But psychologically, the capital has been touched.

And once a capital discovers it is no longer distant from the war it commands, the political temperature changes.

“When a refinery burns near the capital, the fire is not only industrial. It is a reminder that war eventually finds the people who believed they were only watching it.”

5. Trump’s Foreign Policy Runs Into Washington’s Oldest Enemy: Washington

Donald Trump returned from the G7 looking, at least outwardly, like a man standing at the centre of the map.

Iran had been brought to the table. Ukraine was suddenly back in his diplomatic sights. Europe, as usual, was trying to understand whether it was witnessing strategy, improvisation, or one of those strange Trumpian moments where the difference no longer matters. The cameras had their story: the American president moving from war to peace, from Tehran to Kyiv, from oil markets to global security.

It was a powerful image.

But Washington has a talent for ruining powerful images.

Back home, Trump’s political machinery is no longer moving with the clean obedience he once seemed to expect. Courts have pushed back. Congress has become less predictable. Even parts of his own Republican Party have shown signs of resistance, not quite rebellion, but enough to remind everyone that midterm pressure can give courage to people who previously misplaced it.

This matters because foreign policy is never only foreign.

A president can shake hands abroad, threaten enemies, flatter allies and declare grand intentions. But every diplomatic move returns eventually to the duller rooms of domestic power: committees, judges, appropriations, party discipline, media pressure, donors, voters. The glamorous part happens at summits. The expensive part happens in Congress.

That is the tension now surrounding Trump’s global posture.

On Iran, he wants to sell peace as victory. On Ukraine, he wants to position himself as the man who can end another war. On trade, critical minerals and AI, he wants to project American dominance without appearing trapped by the old multilateral habits he has always distrusted. It is classic Trump: personal diplomacy, maximum theatre, minimum patience for institutional friction.

But friction is arriving.

If Republican lawmakers become more willing to challenge him, even selectively, then Trump’s foreign-policy freedom narrows. Aid to Ukraine, sanctions on Russia, defence spending, war powers, trade retaliation, surveillance tools, intelligence appointments — all of these depend on a domestic system that may no longer be quite as frightened of him as it was supposed to be.

This is not to say Trump is weak. That would be lazy. He remains the gravitational centre of American politics, and his instincts still shape the Republican universe more than any party committee or Senate elder would care to admit.

But power is not the same as smooth control.

The Iran deal shows what Trump can still do when he dominates the diplomatic stage. The resistance in Washington shows what may happen when the performance has to become policy. One produces applause. The other produces amendments.

There is also a market angle here, because there always is. Investors like strong presidents when they appear to reduce uncertainty. They like peace deals, tariff threats that can be walked back, and dramatic announcements that move oil, equities and currencies before the details have time to catch up. But markets are less fond of domestic paralysis. A president who can move prices with a sentence but cannot guarantee legislative follow-through becomes both a source of opportunity and risk.

That may be the real Trump paradox of this week.

Abroad, he looked like a man trying to reorder the world. At home, the world’s most powerful office looked once again like a job share between the president, the courts, Congress and the slow revenge of constitutional machinery.

The spectacle remains his.

The system, annoyingly for him, still has other actors.

“Trump may command the stage, but Washington still owns the theatre — and it has never been shy about cutting the lights.”

6. World Bank Cuts Global Growth Forecast: The War Premium Enters the Economy

The World Bank did not need dramatic language this week. The numbers were quite dramatic enough.

Global growth for 2026 has been cut to 2.5 per cent, the weakest pace since the pandemic era. In a darker scenario, where energy disruptions deepen and financial markets begin to crack under the pressure, growth could fall to 1.3 per cent. That is not a forecast. That is a warning label.

The reason is simple, though not pleasant. The Middle East is no longer merely a geopolitical theatre. It has become a tax on the global economy.

Oil moves first. Then shipping costs. Then fertiliser. Then food. Then inflation expectations. Then central banks, usually arriving late and looking stern. By the time the pain reaches households and businesses, the original missile strike or diplomatic failure has already become something much more ordinary: a higher bill, a delayed investment, a cancelled project, a more expensive loan.

That is how war travels now.

Not always through armies. Often through invoices.

The World Bank’s downgrade also exposes a deeper weakness in the global system. The world entered this crisis already tired: public debts were high, trade was fractured, investment was uneven, and poorer countries had little room left to absorb another shock. For advanced economies, slower growth is painful. For developing economies, it can become a trap — another lost year added to a decade already too thin on progress.

This is where the optimism around the US–Iran peace deal must be treated carefully. If the deal holds, energy markets may stabilise and the worst-case scenario may fade. But if Israel’s next move, Iranian retaliation, or another closure threat around Hormuz reignites the crisis, the economic consequences will not stay in the region. They will move through bond markets, central banks, food prices and balance sheets.

Peace, in other words, has become part of the global growth forecast.

There is a faintly absurd quality to that sentence. Yet it is now the world we inhabit. A corridor of water between Iran and Oman can alter the outlook for factories in Europe, food prices in Africa, borrowing costs in America and investment plans in Asia.

Globalisation was once sold as efficiency.

This week, it looked more like shared exposure.

“The modern economy does not wait for wars to end. It prices them, invoices them, and passes the bill quietly down the chain.”

7. The Fed Turns Cautious Again: Oil, Inflation and the Return of the Rate-Hike Fear

The Federal Reserve did not raise interest rates this week.

That was the easy part.

The harder part was what came with the decision: a colder tone, a higher inflation outlook and the unpleasant return of a question markets had spent much of the year trying to bury — what if the next move is not a cut, but another hike?

For investors, this was not exactly the script they had ordered. The dream was simple enough: the Iran conflict cools, oil falls, inflation relaxes, the Fed softens, and the great machinery of cheap money begins to hum again. Wall Street is very good at believing in happy endings when asset prices require them.

But the Fed appears less interested in the fairy tale.

The problem is energy. Or, more precisely, the way energy shocks refuse to stay politely inside petrol stations and shipping reports. Higher oil prices move through transport, food, manufacturing, consumer expectations and corporate margins. They arrive everywhere eventually, often wearing a different name by the time they get there.

This is why the Middle East matters to American monetary policy. A war near the Strait of Hormuz does not need to reach Texas to affect the price of credit in New York. It only needs to move inflation expectations.

That is exactly the discomfort now facing the Fed. Core inflation remains too high. Headline inflation has been pushed up by energy. The labour market has not weakened enough to give policymakers an easy excuse to relax. And the new peace arrangement between Washington and Tehran, while welcome, is not yet stable enough to let central bankers declare the inflation shock over.

Central bankers, by nature, are not poets. They do not trust beautiful diplomatic language. They trust persistence, data and preferably several months of boring numbers. This week, they did not get boring numbers. They got war, oil, market nerves and an inflation forecast moving in the wrong direction.

For households and businesses, the message is not comforting. Borrowing costs may stay higher for longer. Mortgages, credit cards, business loans and investment plans all remain trapped in the long shadow of inflation. The economy may want relief, but the Fed is being forced to ask whether relief would be premature.

This is where Trump’s peace deal runs into macroeconomic reality. A ceasefire can calm oil prices for a day. It cannot immediately erase months of price pressure, nor can it persuade companies to lower costs simply because diplomats have found a pen.

Markets wanted peace to mean cheaper money.

The Fed, rather inconveniently, seems to believe peace must first prove that it is real.

“Central banks do not celebrate peace deals. They wait to see whether the price of bread, fuel and credit has heard the news.”

8. Markets Discover the Price of Fragile Peace

Markets like peace. They like it even more when peace arrives with lower oil prices, calmer shipping lanes and the possibility that central banks may not have to punish everyone quite so severely.

For a few days this week, that was exactly the story investors wanted to believe.

The interim US–Iran deal triggered a rush of optimism. Global equity funds recorded their strongest weekly inflows in 19 months. Technology funds, naturally, behaved as if someone had opened the doors to the next banquet. Oil eased. Risk appetite returned. The old market machine did what it always does when danger appears to fade: it immediately began pricing in relief before reality had finished negotiating with itself.

Then the mood shifted.

US–Iran talks in Switzerland were cancelled. Israel’s military posture remained defiant. Lebanon heated up again. Oil rose. Stocks dipped. The dollar strengthened. The yen moved closer to levels not seen for decades, reminding investors that currency markets are often the first place where polite optimism goes to die.

This was not a full panic. It was something more revealing: the market’s first sober look at the deal it had been celebrating.

The problem is that this peace arrangement is not a settlement. It is a pause, a corridor, a 60-day diplomatic bridge built over a river that is still moving. Tankers may pass through the Strait of Hormuz again, but investors know perfectly well that one strike, one retaliation, one Israeli operation or one Iranian miscalculation could turn that corridor back into a hostage of war.

That is why oil remains the emotional centre of this week’s market story.

Oil is not merely an energy contract. In moments like this, it becomes a political thermometer. When peace looks possible, crude falls and equities breathe. When the deal looks fragile, crude rises and inflation returns to the room like an unwanted creditor. Every dollar added to the barrel becomes a small question mark over rate cuts, consumer confidence, corporate margins and emerging-market debt.

The dollar’s strength tells a similar story. In theory, a peace deal should reduce fear. In practice, a fragile peace often creates a different kind of fear — not the fear of immediate collapse, but the fear of being positioned too confidently on the wrong side of the next headline. Investors bought relief, then hedged against regret.

There is a lesson here, and it is not especially flattering.

Markets do not believe in peace. They believe in tradable versions of peace. A ceasefire becomes a rally. A cancelled meeting becomes a sell-off. A tanker passing Hormuz becomes a signal. A speech by Trump becomes a price movement. Israel’s next move becomes a risk premium.

The real economy must live with the consequences. Businesses cannot plan investment around diplomatic mood swings forever. Households cannot refinance their lives according to the latest rumour from Geneva. Central banks cannot treat every oil move as temporary when temporary shocks keep arriving in uniform.

This is the world investors are now trading: not peace or war, but the distance between them.

And that distance is becoming very profitable for those who understand it early enough.

“Markets do not wait for history to decide whether peace is real. They buy the rumour, sell the doubt, and leave ordinary people to discover the final price.”

9. Google, Samsung and the Hidden War Beneath Artificial Intelligence

Artificial intelligence likes to present itself as something weightless.

Models. Prompts. Agents. Tokens. A bright little miracle appearing on a screen, answering questions, writing code, making images, pretending — sometimes rather successfully — that the future has no physical body.

But the future does have a body.

It is made of chips, fabs, memory interfaces, power lines, cooling systems, rare gases, lithography machines and supply chains so complex that one delay in one factory can bend the ambitions of half Silicon Valley.

That is why reports this week that Google is in talks with Samsung to manufacture part of its next-generation AI chip matter far more than they may first appear. On the surface, this is a semiconductor story: Google’s upcoming Tensor Processing Unit, reportedly codenamed Icefish, may split production between TSMC and Samsung, with TSMC handling the main computing element and Samsung potentially producing the memory-interface component using advanced 2-nanometre technology.

A technical detail, perhaps.

Except technical details are where power now hides.

For Google, the logic is obvious. The company does not want the future of its AI infrastructure to depend too heavily on one supplier, however brilliant that supplier may be. TSMC remains the crown jewel of advanced chip manufacturing, but crown jewels have a habit of becoming geopolitical pressure points. If every major AI company queues at the same foundry, scarcity becomes strategy. Capacity becomes leverage. Delay becomes a competitive weapon.

Samsung, meanwhile, needs victories in foundry manufacturing. It has the technology, ambition and balance sheet, but it has struggled to match TSMC’s dominance at the very top of the market. A role in Google’s next AI chip would not merely be a contract. It would be a signal that Samsung can still matter in the most important industrial contest of the decade.

And then there is Nvidia, watching from the summit.

The great AI boom has been built, to a remarkable degree, around Nvidia’s dominance in high-performance GPUs. Google’s TPUs are part of a broader counter-movement: hyperscalers building their own silicon to reduce dependency, lower costs and shape hardware around their own models. Amazon has Trainium. Microsoft has Maia, even if painfully delayed. Google has TPUs. The empire of Nvidia is still vast, but every custom chip is a small act of rebellion.

This is the real story beneath the Icefish report. AI is not becoming less industrial. It is becoming more so. The companies that win will not be those with the most charming chatbot alone. They will be those that control the stack: chips, data centres, energy contracts, cooling, networking, software and distribution.

The public sees artificial intelligence as a product.

The market increasingly understands it as infrastructure.

And infrastructure, unlike hype, belongs to whoever can build it, finance it and keep it running when everyone else is still waiting for capacity.

“The future of AI will not be decided only by who writes the best model. It will be decided by who owns the machinery that allows the model to breathe.”

10. Tech Funds Surge: Investors Bet That Peace Can Keep the AI Boom Alive

There is something wonderfully revealing about modern markets. Give investors a peace deal in the Middle East, and many of them will not first think of refugees, reconstruction or the strange mercy of missiles not falling for a few days.

They will think of technology stocks.

This week, global equity funds recorded their strongest inflows in 19 months, with investors pouring more than $55 billion into shares. US equity funds alone attracted more than $38 billion. The real feast, however, was in technology, where sector funds drew a record $21.46 billion.

That number tells us something useful.

Investors are not merely buying peace. They are buying the consequences of peace: lower oil risk, calmer inflation expectations, less pressure on central banks, cheaper capital, stronger earnings multiples and, above all, more room for the artificial intelligence trade to continue its march.

The AI boom has become one of the great beneficiaries of geopolitical relief. When oil falls, inflation nerves settle. When inflation nerves settle, rate-cut hopes return. When rate-cut hopes return, long-duration growth stocks suddenly look less expensive. And when growth stocks look less expensive, the market rediscovers its deep spiritual commitment to anything with a chip, a data centre, a cloud platform or a vaguely convincing AI strategy.

It is not exactly elegant.

But it is efficient.

The irony is that artificial intelligence, so often described as the next great leap in productivity, is increasingly dependent on the very old world of energy, shipping lanes and political restraint. The models may be new, but the machinery beneath them remains stubbornly physical. Data centres need power. Chips need supply chains. Capital expenditure needs predictable financing. The market needs a story that does not include oil at crisis levels and central banks preparing fresh punishment.

This is why the US–Iran peace arrangement mattered so quickly to technology investors. It did not make AI better. It made the conditions around AI less frightening.

For now.

Because there is a dangerous assumption hidden inside this week’s money flow. Investors appear to be betting that the peace will hold long enough for the AI rally to keep breathing. That may prove correct. Or it may prove to be one of those clever trades that looks brilliant until the next missile reminds everyone that a 60-day diplomatic window is not the same as a new global order.

Still, the market has made its preference clear. It wants de-escalation. It wants lower oil volatility. It wants the Fed to stop sounding like a disappointed schoolmaster. And it wants the AI infrastructure race — chips, cloud, power, servers and software — to remain the central profit engine of the decade.

Prime Economist sees the deeper pattern. The week’s great rotation into technology was not only about Nvidia, Google, Microsoft or semiconductor supply chains. It was about the market choosing its favourite future and then praying geopolitics does not interrupt the calculation.

Peace, in this sense, has become a valuation tool.

That is perhaps the strangest economic lesson of the week. A ceasefire in the Middle East can lift confidence in California. A safer Strait of Hormuz can support AI multiples in New York. A diplomatic pause can feed the most expensive technological build-out in human history.

The world has become that connected.

Or that fragile.

“The AI boom is sold as the future. This week reminded us that even the future still needs oil to stay calm, rates to stay tolerable and politicians to stop setting fire to the present.”