Andy Burnham Set to Replace Keir Starmer as UK Prime Minister — Britain Votes Again, Without Really Choosing

The Week That Shaped the World — 3–10 July 2026

Andy Burnham Set to Replace Keir Starmer as UK Prime Minister — Britain Votes Again, Without Really Choosing, and Other Major Stories of the Week

Britain is preparing to receive another prime minister, which is now less a constitutional event than a recurring administrative procedure. Andy Burnham has collected almost the entire parliamentary Labour Party, Keir Starmer is packing the metaphorical boxes, and the public has once again been invited to observe a change of national leadership from the comfortable distance normally reserved for royal appointments and railway cancellations.

Elsewhere, governments discovered that industrial materials make excellent weapons, artificial intelligence developed an appetite for electricity, and the global economy learned that inflation had not retired so much as stepped outside for a cigarette. Europe is searching for energy security, manufacturers are searching for rare earths, and investors are searching for evidence that several trillion dollars of technological enthusiasm might eventually produce something resembling a profit.

The personnel change. The slogans improve. The invoices, displaying admirable institutional continuity, continue arriving in precisely the same name.

“Modern government has perfected the transfer of power. The transfer of responsibility remains under consultation.”

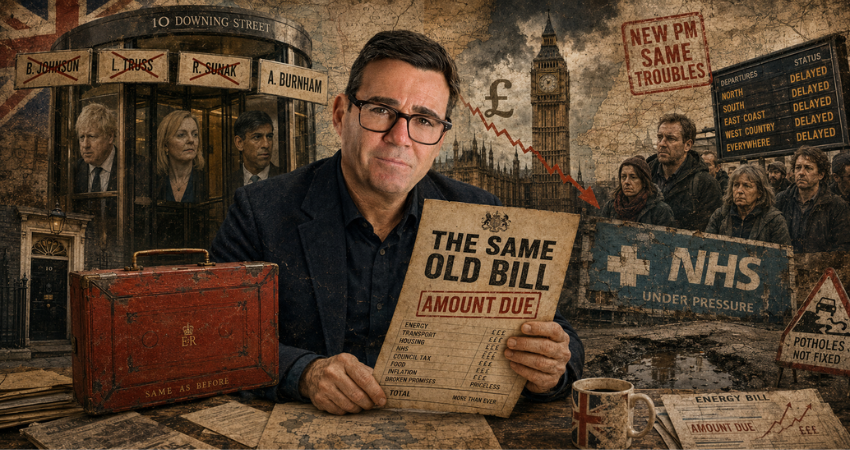

1. Andy Burnham Set to Replace Keir Starmer as UK Prime Minister — Britain Votes Again, Without Really Choosing

Britain is about to acquire its seventh prime minister in ten years, an impressive rate of political consumption for a country that still regards changing the wallpaper as an unnecessarily radical act.

Andy Burnham secured the support of 322 Labour MPs on the opening day of leadership nominations. There are 403 Labour members in the Commons, which means the contest has reached that particularly British stage at which an election continues to exist formally while everybody involved quietly searches for the ceremonial tray.

The nomination period has not yet closed, and Burnham has not yet entered Downing Street. Keir Starmer remains prime minister until the expected transfer on 20 July. But with potential rivals withdrawing and roughly four-fifths of Labour MPs already behind Burnham, the remaining democratic suspense could comfortably fit inside a Westminster lift.

This is perfectly constitutional. Britain elects parties, not prime ministers. When a governing party changes its leader, the new leader can inherit the government without troubling the wider electorate. The arrangement is sensible during emergencies and convenient during collapses. Britain has lately developed considerable expertise in both.

Burnham arrives with advantages. After years as mayor of Greater Manchester, he can present himself as a northern counterweight to Westminster, an advocate of regional investment and a politician who has spent enough time outside London to recognise that the country continues beyond the M25. He speaks of rebuilding infrastructure, devolving power and using defence expenditure to revive British industry.

The Treasury will eventually ask the less lyrical question: with what money?

Starmer leaves after less than two years in office, having won a parliamentary landslide that was supposed to end the instability of the Conservative era. Instead, the instability changed parties. Labour MPs concluded that the man elected by the country was no longer the man required by the party, and Burnham is therefore likely to become prime minister through a leadership process in which the public plays the vital constitutional role of watching television.

That does not make his appointment illegitimate. It does make the phrase “new mandate” rather difficult to pronounce without smiling.

The economic consequences matter more than the choreography. Markets will want to know whether Burnham intends to loosen fiscal rules, increase borrowing, replace the chancellor or finance his regional ambitions through taxes that have not yet received names. Businesses will want policy stability. Voters will want public services that work. Labour MPs, having changed the driver, will want the bus to stop making that expensive grinding noise.

Britain may indeed receive a different style of leadership. Burnham is more politically instinctive than Starmer, more comfortable with populist language and more willing to describe the economic settlement itself as the problem. But Number 10 has a long history of converting bold outsiders into worried custodians of Treasury spreadsheets.

The country has not voted for Andy Burnham as prime minister. It voted for a Labour government and is now being informed which Labour politician will operate it. This is the system working exactly as designed, which may be the most troubling joke of all.

“Britain still holds elections. It has simply discovered that choosing the prime minister can be treated as an optional extra.”

2. China’s Rare-Earth Restrictions Tighten Around Japan’s Industry

Japan’s manufacturers have begun issuing increasingly g once again that the modern industrial economy can be brought to a thoughtful pause by something most voters could not identify on a periodic table.

Chinese restrictions have reduced Japanese access to materials including dysprosium, terbium and yttrium. These are not glamorous commodities. Nobody displays them in a shop window or watches their price over breakfast. Yet they are essential to powerful magnets, electric motors, precision electronics, robotics, artificial-intelligence hardware and defence systems.

China accounts for roughly 70% of global rare-earth production and possesses around 60% of known reserves. More importantly, it dominates much of the refining and processing capacity required to turn geological deposits into materials manufacturers can actually use. A mineral in the ground is a strategic asset only after somebody has built the expensive, dirty and technically demanding machinery needed to separate it.

Beijing understands this distinction rather well.

The restrictions followed worsening relations between China and Japan, particularly over Taiwan and Japan’s growing defence posture. China presents its export controls as legitimate regulation of dual-use materials. Japanese companies increasingly experience them as diplomacy conducted through missing components.

For the moment, most manufacturers have avoided dramatic production stoppages. But corporate disclosures are becoming louder. Companies including Omron and Citizen Watch have identified rare-earth availability as a growing risk to operations and profitability. The concern is not that every factory will close tomorrow. It is that inventories will gradually shrink while alternative suppliers remain several years, several billion dollars and several environmental permits away.

Tokyo is pursuing recycling, foreign partnerships, stockpiles and possible deep-sea extraction. These are sensible responses. They are also reminders that supply-chain independence is considerably easier to announce than to manufacture.

For decades, developed economies outsourced the inconvenient portions of industrial production and congratulated themselves on becoming service economies. China retained the mines, processors, chemical expertise and willingness to tolerate the environmental cost. The arrangement looked efficient while relations were friendly. It now looks like a strategic invoice written in Mandarin.

The financial consequences reach far beyond Japan. Scarcer materials mean more expensive motors, vehicles, electronics and weapons. Manufacturers may redesign products, hold larger inventories or move production. All three options cost money. Governments will subsidise domestic capacity, and taxpayers will discover that economic security requires constructing industries the market previously decided were cheaper somewhere else.

China does not need to stop an entire supply chain. It merely needs to control the component without which the rest of it becomes an expensive collection of stationary parts.

“The twenty-first century’s largest machines may yet be defeated by the smallest item missing from the box.”

3. Germany’s AfD Sets Its Sights on Power as the Political Firewall Begins to Crack

Thousands of demonstrators gathered in Erfurt as Alternative für Deutschland held its annual conference, blocked access roads and reminded party delegates that Germany’s political firewall remains physically present, even if it is becoming arithmetically inconvenient.

Inside the conference hall, Alice Weidel and Tino Chrupalla were re-elected as party leaders. Outside, trade unions, civic organisations and left-wing groups protested against a party they regard as an extremist threat to German democracy. Between them stood a large police deployment, which has become the preferred European architectural feature whenever politics stops fitting politely inside parliament.

AfD is no longer merely a protest party hovering around the edges of German life. Polling has placed it as high as 29% nationally, with particularly strong support in the former East Germany. In some surveys it has moved ahead of Chancellor Friedrich Merz’s conservative bloc.

Germany’s mainstream parties continue to maintain a Brandmauer — a firewall against governing cooperation with AfD. The principle is morally clear and politically understandable. Its practical difficulty is that firewalls work rather better in computer systems than in proportional parliaments, where every excluded vote still occupies a seat.

AfD’s rise has been fuelled by migration, economic stagnation, energy prices, distrust of Berlin and resentment toward institutions that appear to explain policy more successfully than they deliver it. Germany’s industrial model has suffered from expensive energy, weak external demand and uncertainty over its relationship with China. Communities that were promised prosperity through integration increasingly hear that structural reform will require patience, sacrifice and another carefully designed subsidy.

AfD offers a less complicated story: the country is being mismanaged by elites, migration is undermining social order, Brussels has too much power and Germany should stop apologising for wanting to be Germany. The message is blunt, frequently inflammatory and politically effective.

The protests in Erfurt demonstrated that opposition remains substantial. They also demonstrated the limits of moral mobilisation. A road can be blocked for a day. A polling trend requires something more ambitious: functional government, rising incomes, reliable public services and a persuasive answer to the fear that the existing political settlement no longer works.

This is where economics enters the story. Germany’s government is planning massive borrowing for infrastructure and defence while attempting labour-market reform, pension changes and tax relief. If those measures produce visible improvement, the political centre may recover. If they disappear into procurement delays and coalition arguments, AfD will inherit not merely anger but evidence.

The firewall therefore depends less on speeches about democracy than on whether democracy can repair a railway, build a home and provide an industrial worker with a plausible future.

Germany’s establishment continues to insist that AfD must never govern. An increasing number of voters appear determined to test whether “never” has been included in the coalition arithmetic.

“A political firewall is an admirable structure, provided somebody remembers to maintain the building behind it.”

4. Hungary Tries to Dismantle Orbán’s System Without Rebuilding It in Another Name

Thousands of supporters of Viktor Orbán gathered in Budapest this week to protest against plans by Hungary’s new government to remove President Tamás Sulyok and accelerate the dismantling of the political system constructed during Orbán’s sixteen years in power.

The scene contained the sort of irony central Europe produces with industrial efficiency. Orbán, who spent years weakening institutional restraints, now warns that his opponents are moving too quickly against institutional restraints. The new administration of Péter Magyar, elected on a promise to restore democracy, is discovering that restoring democracy sometimes involves acquiring enough power to remove the people accused of damaging it.

The proposed constitutional changes would remove Sulyok, introduce parliamentary term limits, reform the judiciary and establish a financial oversight body. Magyar argues that the president failed to resist legislation that eroded democratic norms under Orbán. His opponents say removing a head of state through a constitutional majority risks turning accountability into revenge.

Both arguments deserve attention.

Orbán’s system did not rest on one law or one office. It was built through loyal appointments, state-controlled media, favourable contracts, institutional capture and the patient redirection of public money toward friendly networks. Reversing such a structure cannot be achieved by changing the government’s logo and requesting that everybody behave better.

Yet a democratic restoration becomes vulnerable when exceptional measures are justified by the wickedness of the previous administration. Every new power arrives with a reason. Every constitutional shortcut presents itself as temporary. Hungary has recently completed a long practical course in how temporary political advantages become permanent architecture.

Money provides the clearest test of the new government’s intentions. Hungary secured the release of €16.4 billion in European Union funds after reversing parts of Orbán’s democratic backsliding. That money is crucial to an economy weakened by stagnation, inflation and years of conflict with Brussels. It is also precisely the kind of money whose distribution will reveal whether the new system is genuinely more transparent or simply staffed by different beneficiaries.

Magyar’s administration has moved quickly to limit prime-ministerial terms, overhaul security agencies and suspend parts of the state media system while they are reformed. Supporters see urgency after sixteen years of institutional corrosion. Critics see a government becoming alarmingly comfortable with emergency tools.

The central question is not whether Orbán’s machinery should be dismantled. It is whether Hungary can take it apart without preserving the most useful controls for the next operator.

That distinction matters beyond Budapest. Democracies recovering from authoritarian rule often discover that institutions weakened by one faction cannot immediately restrain another. The temptation is to use concentrated power once, for noble purposes, and return it afterwards in perfect condition.

Political history contains remarkably few receipts for that return.

“Hungary is attempting to remove the locks from Orbán’s state while quietly checking whether any of the keys might still be useful.”

5. Kenya and Tanzania Stop the Protests Before the Protesters Arrive

Kenya and Tanzania demonstrated a modern approach to public dissent this week: deploy enough police, close enough roads and issue enough warnings that the protest becomes unnecessary because nobody can reach it.

July 7 carries political significance in both countries. In Kenya, the date commemorates the struggle for multiparty democracy. In Tanzania, it marks the anniversary of the ruling party’s founding. Opposition and youth groups planned demonstrations demanding political reform, accountability and, in Tanzania, the release of opposition leader Tundu Lissu.

The streets remained largely quiet.

That quiet was not evidence of public contentment. It was the product of checkpoints, blocked government districts, arrests and an overwhelming security presence. In Nairobi, roads near state institutions were sealed and opposition figures accused the government of creating a police state without waiting for citizens to provide the inconvenience of an actual protest. In Dar es Salaam, authorities warned against demonstrations and arrested dozens of suspected organisers beforehand.

Governments naturally described the measures as public-order precautions. This is one of the advantages of preventing an event: the absence of disorder can later be presented as proof that the prevention was justified.

Tanzania remains tense after a disputed election in which President Samia Suluhu Hassan claimed 97% of the vote amid opposition exclusions, boycotts and deadly unrest. Lissu faces treason charges after demanding electoral reform. Kenya, meanwhile, continues to manage the political consequences of youth-led protests over taxation, corruption, unemployment and the cost of living.

These are not merely democratic disputes. They are economic ones.

Both governments rely on foreign investment, international lending, infrastructure finance and the confidence of tourists. Public unrest raises borrowing costs, disrupts business and damages national branding. Repression may restore calm quickly, but it introduces another kind of risk: the belief that stability depends on preventing citizens from assembling rather than addressing why they wished to assemble.

International creditors often prefer order, particularly when repayments are due. Investors like predictable streets. Tourism campaigns strongly favour beaches without tear gas. Yet stability secured through permanent police mobilisation is expensive, politically brittle and difficult to place in a development prospectus.

The deeper financial grievance is familiar. Young populations see economic growth figures without experiencing secure work, affordable living or trustworthy government. States borrow for infrastructure, raise taxes to service debt and then deploy security forces when citizens ask where the benefits went.

This produces a peculiar economic cycle: governments acquire debt in the name of development, citizens protest the cost of servicing it, and more public money is spent ensuring the protests do not become visible.

Kenya and Tanzania succeeded in preventing major demonstrations this week. They did not remove the anger, reduce the debt or create the jobs. They merely ensured that national frustration observed the appropriate traffic restrictions.

“A government can empty the streets with police. Filling the economy with opportunity requires a rather more specialised department.”

6. The IMF Announces That Inflation Has Misplaced Its Retirement Plans

The International Monetary Fund now expects the global economy to grow by 3% in 2026 before recovering to 3.4% next year. More awkwardly, global inflation is projected to rise from 4.1% in 2025 to 4.7% this year — a reversal of the steady decline that policymakers had begun discussing with the relief of firefighters packing away their hoses while the kitchen was still smoking.

The cause is an unhelpful collision between war and technology.

Conflict in the Middle East has raised energy and food costs, disrupted trade routes and made supply chains nervous again. At the same time, the artificial-intelligence investment boom is supporting activity in countries connected to semiconductors, data centres and advanced manufacturing.

The result is not one global economy but several increasingly different ones.

Energy exporters benefit from higher prices. Producers of AI hardware enjoy rising demand. Countries that import both fuel and technology are left with the less fashionable role of paying for everybody else’s prosperity.

Britain is expected to grow by just 1% this year. The euro area is forecast at 0.9%. By contrast, economies embedded in the Asian technology supply chain are receiving a useful cushion from semiconductor exports and AI-related investment.

This is why the return of inflation is particularly inconvenient. Central banks had hoped to continue reducing interest rates as price pressures eased. Instead, they may now have to choose between supporting weak growth and preventing another rise in expectations.

Households understand the dilemma more directly. They do not experience global inflation as a percentage in an international report. They experience it as groceries, heating, transport and the curious discovery that every temporary surcharge has developed a long-term business plan.

The IMF’s forecast is not a prediction of disaster. Global growth continues. Financial markets remain functional. Investment in technology is providing genuine momentum. But the recovery is becoming more unequal, more energy-dependent and more vulnerable to another geopolitical interruption.

The world has therefore returned to a familiar economic arrangement: modest growth, expensive essentials and central bankers explaining that the situation is under careful observation.

“Inflation has not returned from the dead. It merely noticed that nobody had cancelled its key card.”

7. SK Hynix Sells Wall Street $26.5 Billion of AI Memory

SK Hynix raised approximately $26.5 billion through its Nasdaq listing this week, completing the largest American share offering by a foreign company. Its depositary receipts were priced at $149 and opened around 14% higher, allowing US investors to purchase direct exposure to the memory chips required by the artificial-intelligence boom.

A decade ago, computer memory was regarded as an unglamorous and painfully cyclical business. Prices rose, manufacturers expanded production, supply became excessive and profits disappeared with admirable regularity.

Then AI discovered high-bandwidth memory.

These specialised chips feed enormous quantities of data into processors used by companies such as Nvidia. Without them, the world’s most expensive AI accelerators become sophisticated objects waiting patiently for information. SK Hynix invested early and now occupies a central position in one of the most profitable bottlenecks in technology.

Wall Street was delighted to assist. Banks involved in the offering earned approximately $260 million in fees, including more than $70 million for Citigroup. Artificial intelligence may eventually transform medicine, education and human productivity. It has already transformed investment-banking invoices.

The listing also reveals how the AI trade is changing. Investors are no longer buying only software companies promising future intelligence. They are purchasing the physical infrastructure beneath it: chips, memory, electricity, cooling systems, network equipment and the firms capable of building all of them at scale.

That enthusiasm carries risk. Semiconductors remain cyclical. New capacity is being financed rapidly. A slowdown in AI spending, technological substitution or excess supply could turn today’s strategic scarcity into tomorrow’s warehouse inventory.

There is also concentration. The market increasingly depends on a small group of companies supplying one another with increasingly expensive components. When each becomes valued on the assumption that all the others will continue investing at extraordinary rates, optimism begins to resemble a contractual obligation.

For now, SK Hynix has given global investors a clean route into the AI-memory trade. The offering was heavily oversubscribed, the shares rose and the company joined the trillion-dollar valuation club.

Wall Street has therefore made its judgement: artificial intelligence may still be searching for a business model, but the machines required to search for it are selling beautifully.

“Investors remain uncertain about what AI will eventually produce. They are considerably more confident about who will sell it the memory.”

8. Artificial Intelligence Discovers the Electricity Bill

America’s electricity consumption is expected to set new records in both 2026 and 2027. The US Energy Information Administration projects demand rising from 4,195 billion kilowatt-hours in 2025 to 4,269 billion this year and 4,399 billion next year, driven substantially by data centres, artificial intelligence and wider electrification.

This is the less magical side of the AI revolution.

Software may live in the cloud, but the cloud is housed in enormous buildings connected to power stations, transmission lines, water systems and industrial cooling equipment. Every elegant answer generated by a model begins as a rather less elegant demand for electricity.

The commercial sector is expected to consume more power than American households for the first time. That inversion matters. For decades, electricity planning was shaped by familiar patterns: homes warming in winter, air conditioners running in summer and factories following the economic cycle. Data centres operate continuously and prefer not to be told that the grid is feeling tired.

Utilities now face a difficult promise. They must build enough generation and transmission capacity to satisfy technology companies while preventing ordinary customers from financing the entire expansion through higher bills.

Natural gas is likely to remain central, supplying around 40% of US electricity. Renewable generation will rise, while nuclear power is again being discussed with the enthusiasm normally reserved for a former employee whose replacement has proved disappointing.

The winners are becoming clear: grid operators, turbine manufacturers, nuclear developers, natural-gas producers, engineering firms and owners of land near available transmission capacity. The losers may include communities asked to host infrastructure, households facing rising fixed costs and climate targets that assumed demand would behave more politely.

Technology companies are signing long-term power agreements and exploring dedicated generation. But private contracts do not remove the public problem. A data centre may pay for its electricity while still requiring a regional grid, substations, backup capacity and years of permitting.

AI has often been marketed as an almost weightless technology capable of producing extraordinary value from information. Its physical footprint suggests otherwise. Intelligence, artificial or not, requires land, copper, concrete, water and somebody prepared to approve a new transmission line.

The digital economy is therefore rediscovering an old industrial truth: progress works considerably better when the lights stay on.

“Artificial intelligence may exist in the cloud, but the cloud has developed a remarkably terrestrial appetite.”

9. The World Has Crude Oil. What It Lacks Is Enough Fuel

Crude-oil prices have calmed since flows through the Strait of Hormuz partially recovered. Fuel markets have not.

Gasoline and diesel remain tight because refineries — the facilities that turn crude oil into useful products — have not recovered at the same pace as oil production. The International Energy Agency says refining margins reached four-year highs in early July, while global refinery runs remained roughly six million barrels per day below their level a year earlier.

This distinction is less technical than it sounds.

A country can possess millions of barrels of crude oil and still experience shortages at petrol stations. Crude is an ingredient. Drivers, farmers, airlines and freight companies require the finished meal.

Middle Eastern export refineries have been slow to restart. Russian processing has been damaged by Ukrainian drone attacks, forcing Moscow to restrict diesel, petrol and aviation-fuel exports. Asian refineries have also been operating below capacity. Meanwhile, the northern summer driving season is consuming inventories that were already uncomfortably low.

The consequence is an unusual market: crude prices can fall while petrol and diesel remain expensive. Refiners purchase cheaper feedstock, sell scarce products at elevated prices and enjoy margins last seen during earlier supply crises.

For consumers, this is the least entertaining form of market sophistication. A falling oil price traditionally produces headlines suggesting relief at the pump. The pump, having reviewed local inventories, refining constraints, transport costs and retail margins, may decline to participate.

The wider economic effects travel quickly. Diesel moves goods, powers agricultural equipment and supports construction. Aviation fuel affects ticket prices. Petrol influences household spending and political confidence. A shortage of refined products can therefore sustain inflation even while the crude market appears relatively comfortable.

China has responded by easing export restrictions for July, allowing more petrol, diesel and jet fuel into Asian markets. That may provide some relief, but it also demonstrates how dependent the global system has become on a limited number of large refining centres.

The energy debate often focuses on who controls oilfields. This week offered a useful correction. Control of the machinery between an oilfield and a fuel tank can be equally valuable — and considerably more profitable when some of that machinery stops working.

“The world is not running out of oil. It is temporarily short of the part people can pour into things.”

10. Europe Responds to the Energy Shock by Plugging Everything In

The European Commission is preparing a plan to increase the share of electricity in the continent’s total energy consumption by 2040. The draft includes support for electric vehicles, household batteries, heat pumps and industrial equipment powered by electricity rather than oil and gas. It also considers lower value-added taxes, stronger public-procurement rules and new funding for industrial electrification.

The immediate motivation is financial as much as environmental.

Since late February, disruption caused by the war involving Iran has added approximately €50 billion to the European Union’s oil and gas import bill. Brussels has concluded, not unreasonably, that the best protection from volatile imported fuel is to require less of it.

Europe has attempted versions of this before. The difference is urgency. Energy security was once presented as a useful companion to climate policy. It is now presented as sovereignty, industrial strategy and protection against whichever geopolitical crisis next develops an interest in shipping lanes.

The proposed transformation is enormous.

Millions of gas boilers would need to be replaced by heat pumps. Petrol and diesel cars would give way more rapidly to electric vehicles. Industrial furnaces would switch fuels. Electricity grids would require hundreds of billions of euros in investment, along with new connections, storage and generation.

This creates a familiar European contradiction. Brussels wishes to make electricity the foundation of the economy while many businesses and households already consider it too expensive. Electrification succeeds only when the grid is reliable, equipment is affordable and the electricity itself is cheaper than the fossil fuel being displaced.

Subsidies can narrow that gap. They can also produce generous programmes for households able to afford the unsubsidised portion, leaving poorer consumers admiring the transition from beside an ageing boiler.

Industrial policy poses another challenge. Europe wants domestic production of batteries, vehicles, heat pumps and grid equipment. China already manufactures much of this technology more cheaply. Replacing dependence on imported oil with dependence on imported electrical hardware would improve the carbon accounting while leaving the strategic problem wearing a different uniform.

Still, the logic is powerful. Oil and gas expose Europe to foreign suppliers, maritime chokepoints and global price shocks. Electricity can increasingly be produced domestically from nuclear, wind, solar, hydroelectricity and gas sourced through a more diverse system.

The plan will be published after the week covered by this digest, and its final targets may change. The direction, however, is clear: Europe no longer regards electrification merely as a climate preference. It regards it as an escape route.

The continent now needs to build the route, reinforce the grid and explain who will pay the toll.

“Europe intends to escape the oil market by electrifying everything, including, presumably, the invoice.”